Info [Home]

Why growth rater

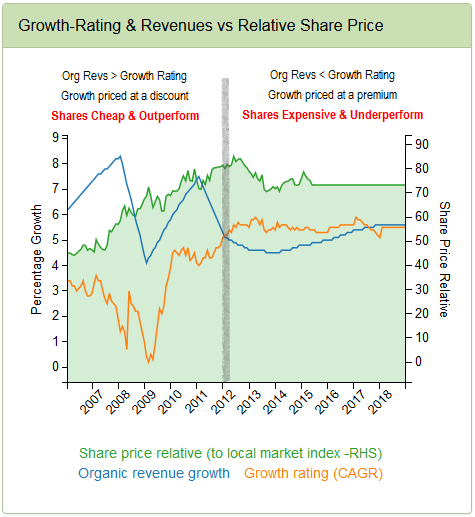

As a financial instrument, an equity’s defining characteristic is its capacity for growth. To gauge its value therefore one must also be able to identify the growth rate that is being discounted by its share price and whether this is commensurate with the trading entity behind it. Markets intuitively recognise this and as we can demonstrate, price accordingly. But do you know what growth is being discounted by the markets on those shares you might buy? Would you be interested to know how sensitive this is to that company’s organic revenue growth and the correlations with key external factors that may influence these? Perhaps you would like to drill down a little deeper to analyse the potential volatility of the valuation by exploring frequency distribution of both revenue and growth rating outcomes and then input your own assumptions to skew the valuation? Perhaps you want volatility as well as growth or perhaps not; that is your choice, but only if you are in a position to make it.

So what’s on offer

Unlike many traditional approaches used by the share pushing industry, the Growth Rater excludes the distorting effects of capital structure (except for tax shields – a la Miller & Modigliani) and uses ‘cleaned up’ data to calculate normalised operating free cash flows and yields from which implied growth ratings can be calculated. Unlike the ubiquitous, but largely meaningless, price to earnings ratio (PER) so beloved by traditional research, a growth rating can be directly related to a group’s historic as well as prospective capacity for growth, in particular organic revenue growth. When viewed through this prism, the systematic relationship between growth delivered and growth priced in by markets can be quantified; and yes markets appear quite rational in the way they price in growth to stocks! A systematic relationship however is only relevant to an investor if it can be used as part of a predictive tool, including dynamic sensitivity analysis tools and this is where the Growth Rater really joins up the dots.

Analysis tools include:

- A 5 point correlation analysis of stock metrics against a wide range of international macro data. Correlation is not causation, but will still help flag the top factors that may have influenced the way the share price performed, the valuation expectation placed on it by the market or perhaps had a direct impact on the group’s trading performance, such as organic revenue growth and margins.

- Valuation sensitivities: Predictive tools on assessing the volatility in prospective valuations with full analysis on historic ranges for organic revenues and rating, including user selection options for date and confidence intervals as well as for changing revenue growth assumptions or drop-thru ratios. A prospective upside to a valuation target is simple enough, but one still needs to be able to quantify ones valuation risk on objective metrics to balance the risk/reward equation within one’s own chosen investment parameters.

- Mean reversion: A particularly powerful tool for accommodating stocks while in very high growth mode – ‘super growthers’. This includes a correlation analysis between organic revenue growth and the forward reach to bring the growth rating back to a market average. This algorithm is integral to the growth rater methodology and also provides a digestible graphical explanation of how markets have been valuing these groups.

- Comps: a series of 9 charts providing key valuation and performance data by stock including the respective sector comparative and also that for the overall Growth Rater coverage universe. As the WYT data is standardised to include items such as stock compensation and discontinued operations until actually sold, but exclude non-trading items such as disposal gains, this ‘cleaned up’ can provide a robust perspective on some of the broader market metrics which can either be used to validate the top down estimates or those from other providers that aggregate company data as supplied.

Independent

Not just independent, but because it is based on a structured valuation system, it also limits the propensity to goal seek often found in investor research.

Market neutral

It is market neutral. We do not impose our view of the relative merits of equities over other asset classes into our equity valuations. We calculate and use equity risk premiums and cost of capital data within our system and monitor relative returns across differing macro assumptions; features that we intend to offer to users in future upgrades. There is no ‘right’ or ‘wrong’ equity risk premium however, merely what the balance of fear, greed and central bank manipulation may make it at any given time. Our aim is to empower investors with insight into what that is, or might become rather than join the boom and gloom merchants. Stock valuations therefore are made on a market relative basis.